A few years ago, banking meant forms, queues and fixed timings. Now, your phone handles most of your banking needs. With UPI, mobile apps and digital tools growing across India, banking has become faster, simple and fully online.

In this change, NEO Banks are getting attention. They are making banking easier for young users, small business owners, freelancers and even startups that want everything fast. This guide will explain what NEO Banks are, how they work in India, the best features, risks, and how to pick one confidently.

What is a Neo Bank

A NEO Bank is a bank that works mainly through mobile apps or websites.

Some quick points:

- You do not need a physical branch

- You can open accounts using your phone

- UPI, payments and cards are included

- Focus on smooth user experience

They aim to reduce fees and remove old-style banking delays.

How NEO Banks Are Different From Normal Online Banking

Traditional banks give online access, but they still depend a lot on branches. NEO Banks are created as digital-first. They focus completely on app-based experience and faster service.

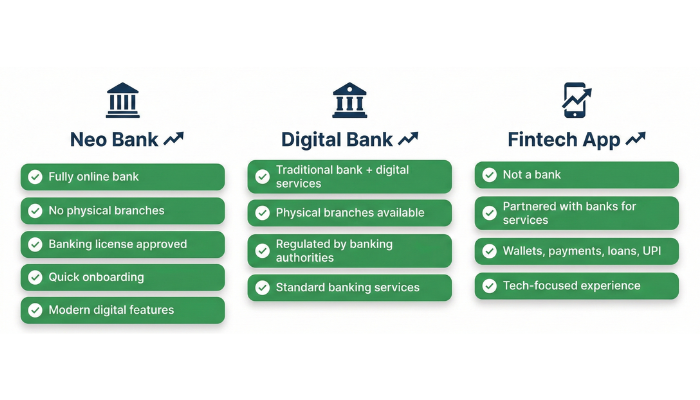

Neo Bank vs Digital Bank vs Fintech App

| Type | Meaning | Services | Physical branch |

| Neo Bank | Fully app-based banking-like service partnering with licensed banks in India | Accounts, cards, UPI, payments | No |

| Digital Bank | A licensed traditional bank that provides major services digitally may or may not have branches depending on country and model | Loans, deposits, cards, support | Sometimes |

| Fintech App | Not a full bank but offers other financial tools | Wallet, UPI, investments | No |

So NEO Banks sit between full banks and financial apps. Simple, clean and easy for users who are always on mobile.

How Neo Banks Work in India

App First, Branchless Banking Model

- Everything happens through the app.

- No paperwork. No waiting lines.

- A phone and internet are enough.

Partner Bank Model in India

In India, NEO Banks do not have their own banking license yet. They operate with partner banks that are regulated by RBI.

So:

- NEO Banks give a modern tech interface

- Partner bank handles your deposits safely

This is why the Indian model is trusted but controlled.

Use of APIs, Cloud And Modern Systems

They use:

- Cloud computing

- Secure APIs

- Updated core banking systems

That means faster response, clear dashboards and fewer errors.

Online KYC And Instant Account Opening

You can open accounts using:

- Aadhaar e-KYC

- PAN verification

- Video KYC

Even older people who are new to online banking find it simple.

Flow of Money Between Bank, Card And UPI

All your money stays safely in the partnered licensed bank.

The app connects:

- Balance

- Card payments

- UPI transfers

- Bills

The app gives full control on one screen.

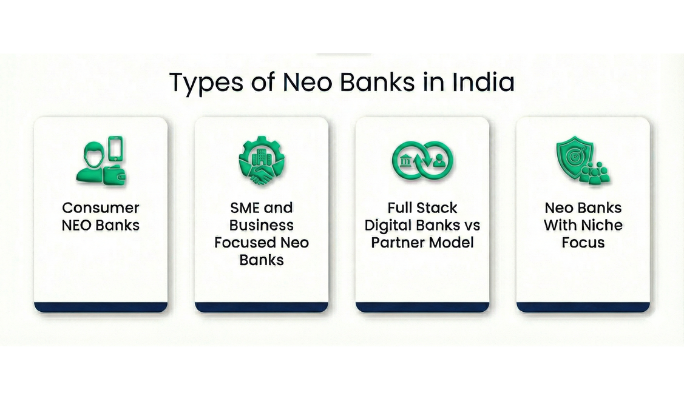

Types of Neo Banks in India

Consumer NEO Banks

These provide daily personal services:

- Savings and salary accounts

- Cards and UPI

- Smart spending tools

Good for anyone who likes simple digital finance.

SME and Business Focused Neo Banks

These help business users manage money easily:

- Current accounts

- Vendor payouts

- Staff expense cards

- Accounting support

Great for startups and small shops.

Full Stack Digital Banks vs Partner Model

- In India today, NEO Banks work through partnerships

- Full digital bank licenses have not been issued yet by RBI

So the partner model continues for safety and regulation.

Neo Banks With Niche Focus

Some NEO Banks target:

- Students

- Gig workers

- MSMEs

- Remote workers

- NRIs

They design features for their daily needs.

Neo Banks vs Traditional Banks in India

| Feature | NEO Banks | Traditional banks |

| Access | App only | Branch and app |

| Account opening | Fully online | Often branch visit required |

| Speed | Very quick | Slower for some services |

| Charges | Low or zero | Extra fees are common |

| Wealth and loans | Limited | Wide |

| Trust | New but improving | Very strong |

| Support | Chat or phone | In person and by phone |

NEO Banks win in speed and simplicity while traditional banks win in history and full services.

Key Features and Services Offered by Neo Banks

Here is what users usually get:

- Digital savings and current accounts

- Physical and virtual cards

- UPI payments, transfers and bills

- 24×7 access with real-time alerts

Smart tools many people love:

- Spend tracking and category insights

- Notification for every swipe

- Goal-based savings and auto rules

- Short term credit, like salary advances

For business accounts:

- Payout automation

- GST billing and invoicing

- Staff cards and spending limits

- Accounting software integration

Everything is focused on helping users take better control of money.

Are Neo Banks Safe in India

Who Protects The Money

Since deposits are held by a licensed bank, security standards are high.

RBI controls the partner bank.

Deposit Insurance

If the partner bank offers deposit insurance, that protection applies automatically.

Always check which bank holds your money.

Security in the apps

NEO Banks Use:

- Encryption

- Biometric login

- OTP verification

Good habits like secure passwords are still important.

If The App Stops Working

Funds remain in the licensed partner bank.

User access may shift but money does not vanish.

Avoiding Risky Services

Check:

- Partner bank name clearly shown inside the app

- Transparent fees

- Genuine offers (nothing too crazy)

- Good history and reviews

If you are unsure, start small.

How Neo Banks Make Money

They keep costs low, since no branches means lower spending. Their income comes from:

- Card interchange fees

- Subscription plans for extra features

- Commissions from insurance, credit and investments

- Interest share from lending by partner bank

- Payment transaction revenue for business users

- Embedded finance and data insights to partner companies

This allows them to offer helpful services at better prices.

Benefits of Neo Banks for Indian Users

NEO Banks can be the best choice for people who love everything digital.

Benefits include:

- Fast sign-up with no other paperwork

- Very low fees or no minimum balance

- More control with real-time alerts

- Spend tracking that helps budget better

- Easy for gig workers and remote jobs

- Works well for people in smaller towns with fewer branches

More people in India are shifting to this experience.

Limitations and Risks of Neo Banks

There are some things to keep in mind:

- No branch support for complex issues

- Depends totally on app and internet

- Not all big loans or wealth services are available

- Many brands are new which affects trust

- Data safety must always be checked

It is smart to use it carefully and stay aware.

Major Neo Banks in India (Quick View)

| Neo Bank | Focus Area | Partner Banks / Institutions |

| Fi Money | Young salaried people | Federal Bank |

| RazorpayX | Business and startups | RBL Bank, Axis Bank, YES Bank, ICICI Bank, SBM Bank, Equitas SFB, Kotak Bank |

| Jupiter | Easy everyday banking | Federal Bank |

| Niyo | International and online spending | DCB Bank, SBM Bank, YES Bank, ICICI Bank |

| Open | SME money management | ICICI Bank, YES Bank and others |

| Freo | Credit-based funding solutions | IDFC FIRST Bank, RBL Bank, YES Bank plus NBFC partners like DMI Finance, Credit Saison, etc. |

Always check updated partner details before transferring large amounts.

RBI Regulations and Policy View on Neo Banks

- NEO Banks in India do not have full banking licenses

- They must operate through regulated traditional banks

- RBI focuses strongly on customer safety and data protection

- KYC rules and digital onboarding guidelines are required

- Account Aggregator system will improve secure data sharing

No full digital-only licensed bank exists in India yet. But the ecosystem continues to grow fast.

How to Choose the Right Neo Bank in India

A simple checklist:

- Confirm partner bank name and RBI link

- Check deposit insurance details

- Read fees and fine print

- Look at app rating and user feedback

- Match features with your need like business, travel or daily savings

- Test with small deposits first

Good research saves future trouble.

Future of Neo Banks and Digital Banking in India

India is already a global leader in mobile payments. NEO Banks will grow more because:

- UPI and cashless habits rising everywhere

- Young users prefer online money tools

- AI will help with automated insights and safer finance

- More embedded finance will connect cards, spending and investments easily

- Support for small business and startups will expand through better funding access

Full digital bank licenses are still not allowed, but innovation will continue through the partner model.

Practical Use Cases for Indian Users

You can try NEO Banks in different ways:

- As your main salary or savings account if you are comfortable with online banking

- For travel or other international needs using global cards

- As a business account to control payouts and expenses

- As a side account to track spending separately or try offers

Move step by step and see what fits your lifestyle.

Conclusion

NEO Banks are changing how people manage money in India. They offer faster service, less paperwork and better control through simple apps. They are especially helpful for young professionals and startups who want freedom from old branch-based systems.

Still, traditional banks remain strong for full services and trust. So the smart approach is to use NEO Banks where they shine, and keep important long term funds safe with trusted institutions.

As India keeps growing with digital payments and new finance ideas, NEO Banks will continue to become a bigger part of daily life.

FAQs

Q. Do NEO Banks follow RBI rules and guidelines?

Yes. NEO Banks in India must follow RBI rules, but they do this through their partner banks. The partner bank is fully regulated, and NEO Banks must meet strict security and compliance standards.

Q. Are NEO Banks safe in India?

They are generally safe because customer money is stored with licensed partner banks under RBI supervision. Still, safety depends on choosing trusted NEO Banks with strong security and clear policies.

Q. Do NEO Banks give deposit insurance in India?

Deposit insurance depends on the partner bank. If that bank has DICGC insurance, the same protection applies to your NEO Bank account, up to the allowed coverage limit.

Q. Which NEO Bank is best for daily online payments?

Different users prefer different apps, but popular choices include Fi Money, Jupiter and Niyo. They provide smooth UPI, cards, fast support and low fees for everyday online payments and spending.

Leave a Reply